G7 - Review Lesson 3

Presentation

•

Social Studies

•

7th Grade

•

Medium

Muhammad Agung Darlianto

Used 4+ times

FREE Resource

0 Slides • 45 Questions

1

Multiple Choice

2

Multiple Choice

3

Multiple Choice

4

Multiple Choice

5

Multiple Choice

6

Multiple Choice

7

Multiple Choice

8

Multiple Choice

9

Multiple Choice

10

Multiple Choice

11

Multiple Choice

12

Multiple Choice

13

Multiple Choice

14

Multiple Choice

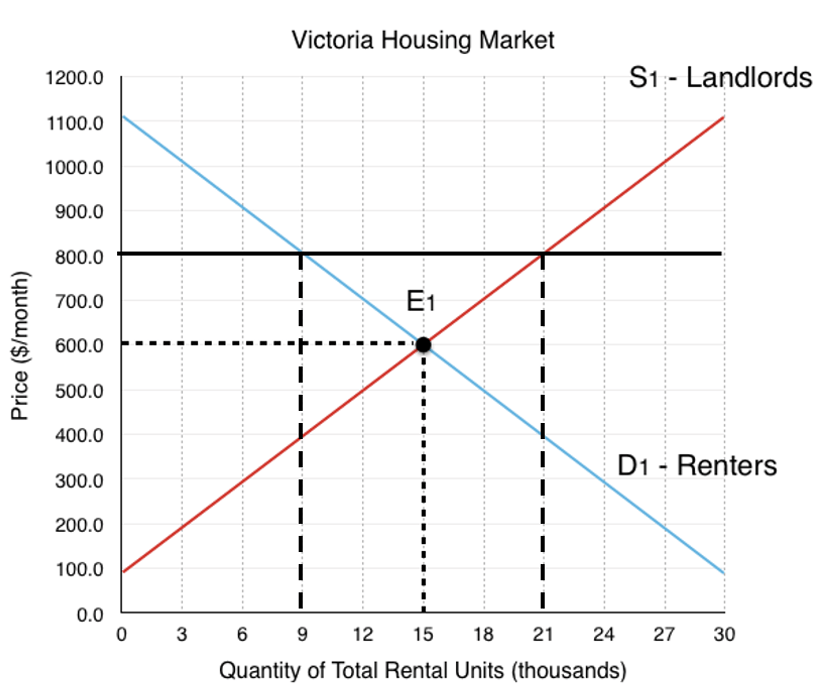

If the current price is $800, which of the following would be the best description for the situation that exists in the market

15

Multiple Choice

16

Multiple Choice

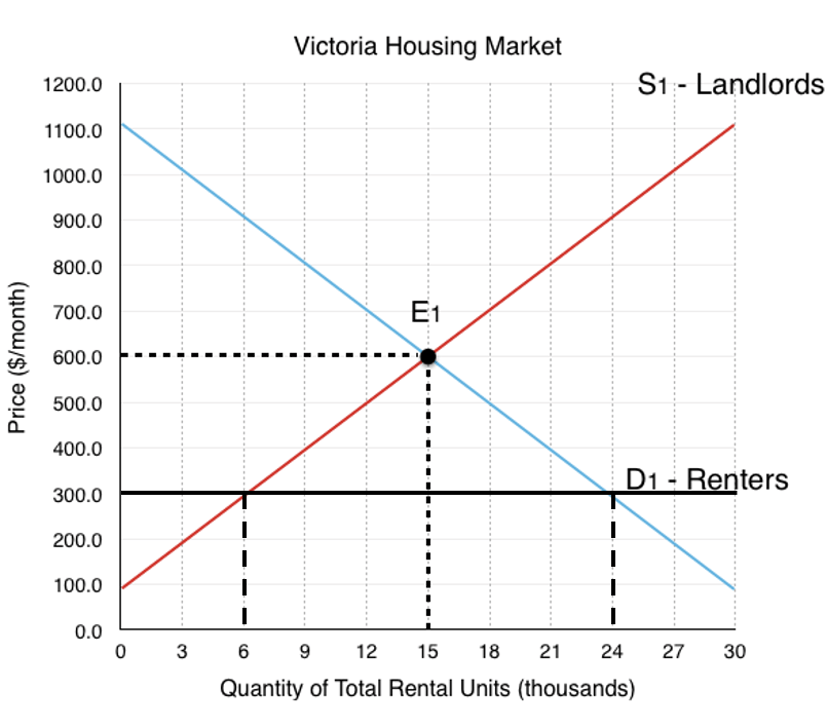

If the current price is $300, which of the following would be the best description for the situation that exists in the market

17

Multiple Choice

18

Multiple Choice

19

Multiple Choice

20

Multiple Choice

21

Multiple Choice

22

Multiple Choice

23

Multiple Choice

24

Multiple Choice

25

Multiple Choice

Refer to Graph 4-1. The movement from point A to point B on the graph shows

26

Multiple Choice

27

Multiple Choice

28

Multiple Choice

What happens to the market when the chocolate bars are priced at $4 each?

29

Multiple Choice

30

Multiple Choice

What happens to the market when the chocolate bars are priced at $1 each?

31

Multiple Choice

32

Multiple Choice

33

Multiple Choice

Refer to Graph 4-4. On the graph, what could most likely cause the movement from S to S1?

34

Multiple Choice

35

Multiple Choice

Refer to Graph 4-5. According to the graph, what are the equilibrium price and quantity?

36

Fill in the Blanks

37

Multiple Choice

Refer to Graph 4-5. According to the graph, What occurs at a price of $7?

38

Open Ended

39

Multiple Choice

Refer to Table 4-2. In the table shown, what would be the result if the price were $8?

40

Multiple Choice

41

Multiple Choice

42

Fill in the Blanks

43

Open Ended

44

Open Ended

45

Multiple Choice

Show answer

Auto Play

Slide 1 / 45

MULTIPLE CHOICE