Free Printable Debt to Income Ratio Worksheets for Class 12

Class 12 debt to income ratio worksheets from Wayground help students master personal finance concepts through comprehensive printables, practice problems, and answer keys that build essential economic literacy skills.

Explore printable Debt to Income Ratio worksheets for Class 12

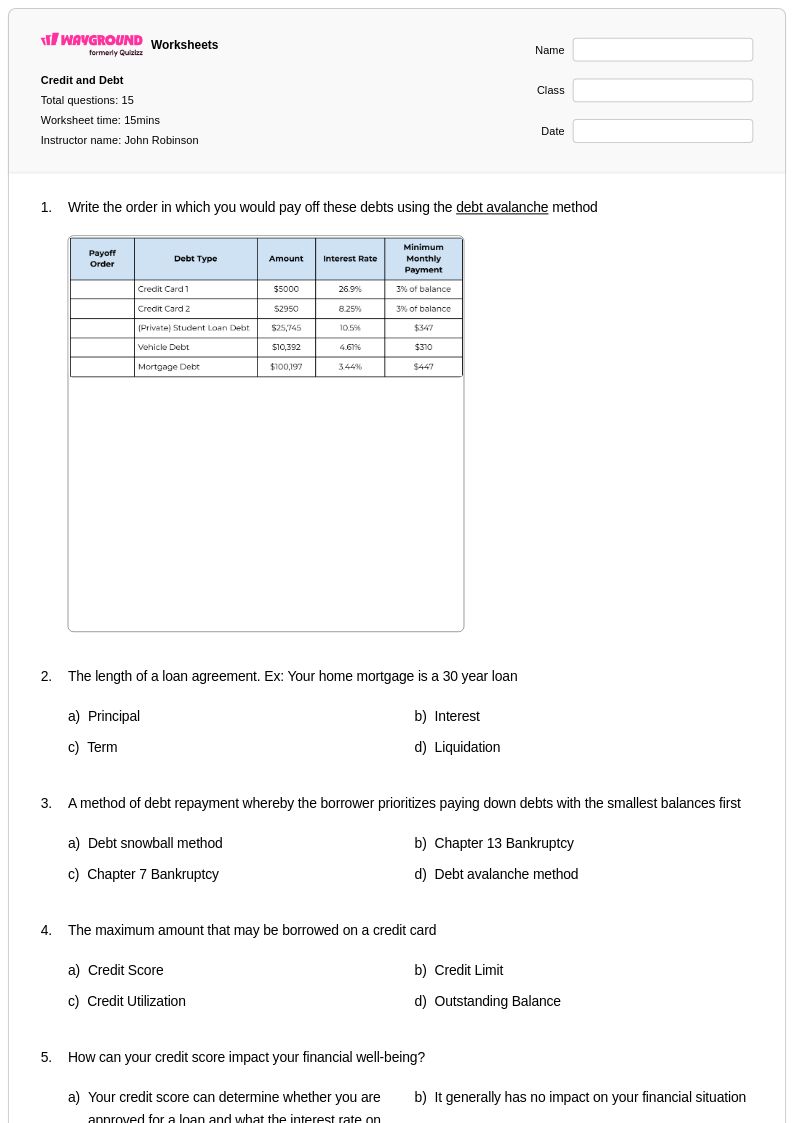

Debt to Income Ratio worksheets for Class 12 students provide essential practice in calculating and interpreting this critical financial metric that measures an individual's monthly debt payments against their gross monthly income. These comprehensive worksheets guide students through real-world scenarios where they analyze various debt obligations including credit cards, student loans, mortgages, and car payments to determine financial health and lending eligibility. Students strengthen their mathematical reasoning skills while mastering percentage calculations and developing practical financial literacy competencies through structured practice problems that mirror actual lending industry standards. Each worksheet includes detailed answer keys and step-by-step solutions, with free printable pdf formats that allow students to work through multiple examples ranging from basic ratio calculations to complex financial planning scenarios involving multiple income sources and debt types.

Wayground, formerly Quizizz, empowers educators with millions of teacher-created resources specifically designed to support comprehensive debt to income ratio instruction for Class 12 economics courses. The platform's robust search and filtering capabilities enable teachers to locate worksheets that align with state financial literacy standards while offering differentiation tools that accommodate diverse learning needs and skill levels within the classroom. Teachers can customize existing worksheets or create entirely new materials, with flexible options for both printable pdf distribution and interactive digital formats that facilitate immediate feedback and progress tracking. These extensive worksheet collections support varied instructional approaches including direct instruction reinforcement, targeted remediation for struggling students, and enrichment activities for advanced learners, ensuring that all students develop the quantitative skills and financial awareness necessary for making informed economic decisions throughout their lives.

FAQs

How do I teach debt to income ratio in a personal finance class?

Start by establishing what counts as debt versus income, since students often confuse gross and net income when setting up calculations. Introduce the formula (total monthly debt payments divided by gross monthly income, expressed as a percentage) using relatable examples like a first-time renter or car loan applicant. From there, connect the math to real-world thresholds lenders use, such as the common guideline that a DTI above 43% typically disqualifies a borrower from a qualified mortgage. This context gives students a reason to care about the calculation beyond the arithmetic itself.

What practice problems work best for teaching debt to income ratio?

Scenario-based problems are most effective because they force students to identify which expenses qualify as debt and which do not before performing any calculation. Effective practice problems present a full financial snapshot, including monthly income, rent or mortgage payments, car loans, student loans, and credit card minimums, and ask students to determine whether a lender would approve the borrower. Graduated problem sets that begin with straightforward single-debt scenarios and build toward complex multi-debt profiles help students develop calculation fluency before tackling interpretation questions.

What mistakes do students commonly make when calculating debt to income ratio?

The most frequent error is using net (take-home) income instead of gross monthly income in the denominator, which inflates the DTI percentage and leads to incorrect conclusions about a borrower's financial health. Students also commonly include non-debt expenses like groceries or utilities in the numerator, not understanding that DTI only counts recurring debt obligations. A third common mistake is failing to convert annual income to a monthly figure before dividing, producing a ratio that is off by a factor of twelve.

How can I use debt to income ratio worksheets to support students at different skill levels?

For students who are still building arithmetic confidence, start with problems that provide pre-calculated monthly totals so the focus stays on setting up and interpreting the ratio rather than multi-step arithmetic. Advanced students benefit from open-ended scenarios where they must recommend whether a borrower should pay down specific debts before applying for a loan. On Wayground, teachers can apply accommodations such as reduced answer choices or read-aloud support to individual students, allowing the same worksheet to serve a differentiated classroom without requiring separate materials.

How do I use Wayground's debt to income ratio worksheets in my classroom?

Wayground's debt to income ratio worksheets are available as printable PDFs for traditional classroom use and in digital formats for technology-integrated environments, including the option to host them as a quiz directly on Wayground. Each worksheet includes complete answer keys, so teachers can use them for guided practice, independent work, or assessment without additional preparation. The platform's search and filtering tools allow instructors to quickly locate worksheets that match specific learning objectives, making lesson planning more efficient.

How does debt to income ratio connect to broader personal finance and economics standards?

Debt to income ratio sits at the intersection of several personal finance competencies, including budgeting, credit management, and understanding lending criteria, making it a high-leverage topic in financial literacy curricula. Teaching DTI gives students a concrete, quantitative tool for evaluating borrowing decisions, which connects directly to standards around responsible credit use and long-term financial planning. Because the calculation requires students to categorize income and expenses accurately, it also reinforces foundational budgeting skills taught earlier in a personal finance course.