- Resource Library

- Social Studies

- Economics

- Supply And Demand

- Chapter 3: Honors Econ Supply And Demand Review

Chapter 3: Honors Econ Supply and Demand Review

Presentation

•

Social Studies

•

12th Grade

•

Medium

Michael Phillips

Used 3+ times

FREE Resource

71 Slides • 140 Questions

1

2

3

Multiple Choice

4

5

6

7

Multiple Choice

8

9

Multiple Choice

10

11

Multiple Choice

12

13

Multiple Choice

14

15

Multiple Choice

16

17

Multiple Select

18

19

20

21

22

23

24

25

Open Ended

26

Open Ended

27

28

Open Ended

29

30

Multiple Choice

31

Open Ended

32

Open Ended

33

Multiple Choice

34

Open Ended

35

36

37

38

39

Multiple Select

40

41

42

Multiple Choice

43

44

Multiple Choice

45

46

47

Multiple Choice

48

49

Multiple Choice

50

Multiple Choice

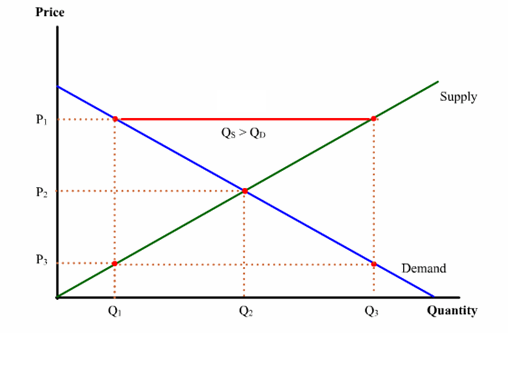

When the supply of a product or service goes up and the demand stays the same the Price will typically do what?

51

52

Multiple Choice

53

54

55

56

57

Open Ended

58

Open Ended

59

Multiple Choice

Which graph below shows the SUPPLY CURVE?

60

Open Ended

61

62

63

64

65

Multiple Choice

66

67

68

69

70

Open Ended

71

Open Ended

72

Open Ended

73

Open Ended

74

75

76

77

78

Multiple Choice

79

Multiple Choice

80

81

82

Open Ended

83

Multiple Choice

84

Multiple Choice

85

Multiple Choice

86

Multiple Select

87

88

89

Open Ended

90

91

Open Ended

92

93

94

95

Multiple Choice

96

Multiple Choice

97

Multiple Choice

When the supply of a product or service goes up and the demand stays the same the Price will typically do what?

98

99

100

Multiple Choice

Which graph below shows the SUPPLY CURVE?

101

102

103

Multiple Choice

104

Multiple Choice

105

106

107

108

109

110

Multiple Choice

The diagram represents a(n)

111

112

113

Multiple Choice

114

Multiple Choice

115

Multiple Choice

116

117

118

Multiple Choice

119

120

Multiple Select

121

122

Multiple Choice

123

124

Multiple Select

125

126

Multiple Choice

127

Multiple Choice

128

Multiple Choice

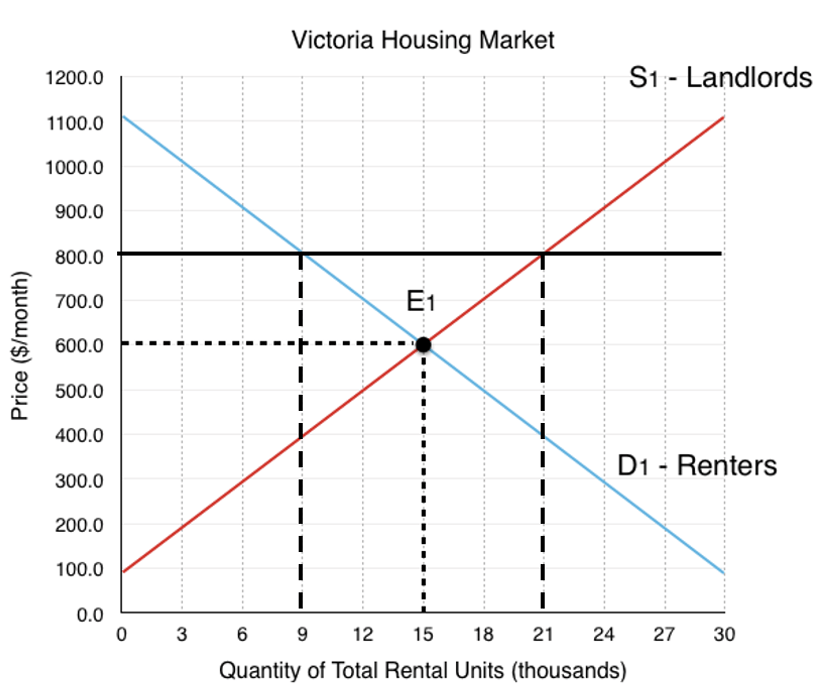

If the current price is $800, how many houses will be sold?

129

Multiple Choice

If the current price is $300, how would market equilibrium be restored?

130

Multiple Choice

If the current price is $300, which of the following would be the best description for the situation that exists in the market

131

Multiple Choice

If the current price is $800, which of the following would be the best description for the situation that exists in the market

132

Multiple Choice

Which statement below would be the most correct to describe the equilibrium quantity ?

133

Multiple Choice

Which statement below would be the most correct to describe the equilibrium price?

134

Multiple Choice

135

Multiple Choice

136

Multiple Choice

Does the red line located on the graph represent a price ceiling or price floor?

137

Multiple Choice

Suppose that the market for coats is described as follows: What is the equilibrium price of coats?

138

Multiple Choice

139

Multiple Select

140

Multiple Choice

141

Multiple Choice

142

Multiple Choice

Which statement is correct about the Law of Demand?

143

Multiple Choice

Which statement is correct about the Law of Supply?

144

Multiple Choice

145

Multiple Choice

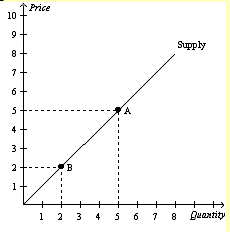

The movement from Point A to Point B represents a(n)

146

Multiple Choice

What does this graph show?

147

Multiple Choice

148

Multiple Choice

149

Multiple Choice

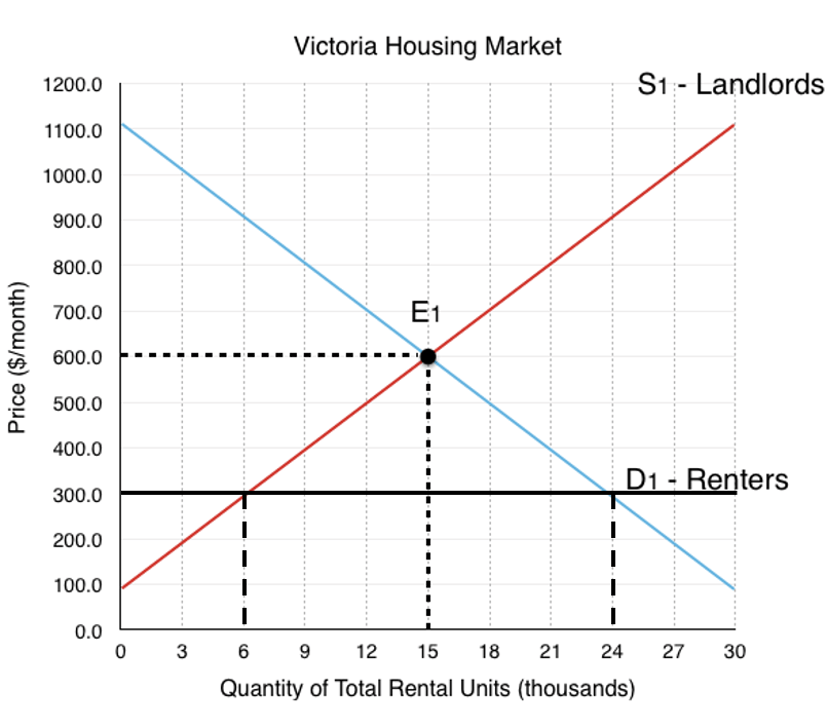

If the current price is $300, how many houses will be sold ?

150

Multiple Choice

If the current price is $800, how will market equilibrium be restored?

151

Multiple Choice

If the current price is $300, which of the following would be the best description for the situation that exists in the market

152

Multiple Choice

If the current price is $800, which of the following would be the best description for the situation that exists in the market

153

Multiple Choice

Which statement below would be the most correct to describe the equilibrium quantity ?

154

Multiple Choice

Which statement below would be the most correct to describe the equilibrium price?

155

Multiple Choice

156

Multiple Choice

157

Multiple Choice

Suppose the government sets a price ceiling of $80. How large will the shortage be?

158

Multiple Choice

Suppose that the market for coats is described as follows: What is the equilibrium price of coats?

159

Multiple Choice

160

Multiple Select

161

Multiple Choice

162

Multiple Choice

163

Multiple Choice

164

Multiple Choice

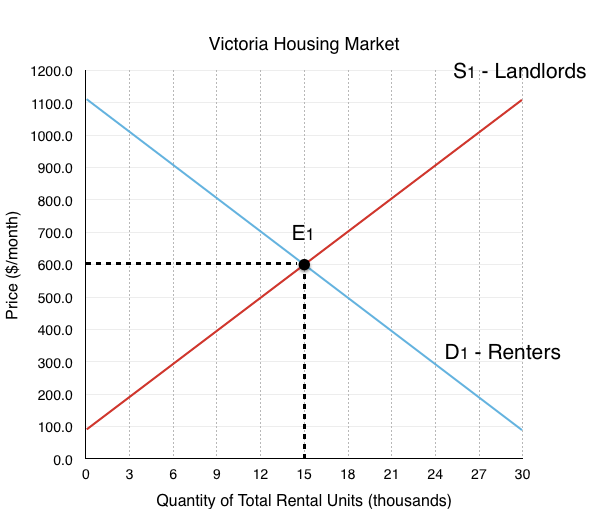

What is the Equilibrium Quantity?

165

Multiple Choice

What is the Equilibrium Price?

166

Multiple Choice

Is the blue line located in the graph representing a price ceiling or price floor?

167

Multiple Choice

Which statement is correct about the Law of Demand?

168

Multiple Choice

Which statement is correct about the Law of Supply?

169

Multiple Choice

170

Multiple Choice

The movement from Point A to Point B represents a(n)

171

Multiple Choice

What is the Equilibrium Price?

172

Multiple Choice

What does this graph show?

173

Multiple Choice

174

Multiple Choice

The desire or willingness a consumer has to purchase a good or a service is called?

175

Multiple Choice

What does this curve represent?

176

Multiple Choice

What does this curve represent?

177

Multiple Choice

178

Multiple Choice

179

Multiple Choice

180

Multiple Choice

181

Multiple Choice

182

Multiple Choice

183

Multiple Choice

184

Multiple Choice

At which quantity does supply and demand reach equilibrium?

185

Multiple Choice

At which price is equilibrium?

186

Multiple Choice

What does this curve represent?

187

Multiple Choice

188

Multiple Choice

189

Multiple Choice

190

Multiple Choice

191

Multiple Choice

192

Multiple Choice

193

Multiple Choice

194

Multiple Choice

At which quantity does supply and demand reach equilibrium?

195

Multiple Choice

196

Multiple Choice

197

Multiple Choice

198

Multiple Choice

199

Multiple Choice

200

Multiple Choice

Refer to Table 4-2. In the table shown, what would be the result if the price were $8?

201

Multiple Choice

Refer to Graph 4-5. According to the graph, What occurs at a price of $7?

202

Multiple Choice

Refer to Graph 4-5. According to the graph, what are the equilibrium price and quantity?

203

Multiple Choice

204

Multiple Choice

205

Multiple Choice

206

Multiple Choice

Refer to Graph 4-1. The movement from point A to point B on the graph shows

207

Multiple Choice

208

Multiple Choice

209

Multiple Choice

210

Multiple Choice

211

Multiple Choice

Show answer

Auto Play

Slide 1 / 211

SLIDE